February 2019 Market Update

February 28, 2019Market Update as of May 15th, 2019

May 29, 2019

As we end March and head into April, we wanted to keep you abreast of the happenings in the economy and how it relates to the market and your money.

- The S&P 500 is up 12.84%, the Barclay’s US Bond Index is up 3.04% YTD and the MSCI All Country World Index (ACWI) is up 10.86% for the year.

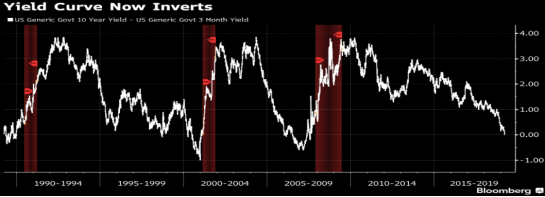

- The 10-year treasury hovers around 2.386%, recently inverting with the 3-month Treasury Yield at 2.422% and raising fears of a recession.

- The Federal Reserve stated that they are taking a “wait and see” stance on any future interest rate increases for the rest of 2019.

- The Mueller Russian collusion investigation has come to an end with no indictments on anything other than process crimes, adding to domestic market stability.

- Trade tariff talks with China are still hanging over US market as a Summit between Trump and Xi Jinping initially set for late March, then delayed until April, has now been pushed back to June.

- Internationally, a successful Brexit compromise in the UK parliament remains elusive.

- Global growth continues to slow, possibly signaling the start a domestic slowdown.

- WTI Crude oil is up over 30% this year to ~$60/bbl but well off its October 3rd, 2018 high of $76.41/bbl as turmoil in Venezuela is partially to blame for the recent increases.

- Fluent Financial has taken a more conservative stance in our portfolios since mid-February, increasing our overall cash holdings and adding downside Put protection as risks appear greater for the US market to make a downside versus upside surprise move.

US Markets have been rangebound over the last few weeks and appears to be taking a “wait and see” attitude towards possible market moving events. The S&P 500 Index is up close to 13% this year but over 11% of these gains occurred in January and February. Still, this ranks as the best quarterly performance since 2009 and the best first quarter performance since 1998. Much of the volatility we saw in December of 2018 through the first part of 2019 has calmed down as the Federal Reserve takes a more “dovish” stance by backing away from a previously announced rigid interest rate hike schedule. 2019 had originally priced in two rate hikes but analysts now predict zero rate increases this year. “Inflation is muted and our policy rate we think is in an appropriate place,” Powell said in an interview that aired March 10th on CBS News’ “60 Minutes.” He called the current rate setting “roughly neutral” and tried to define the Fed’s stance of patience while reviewing fresh data. “Patient means that we don’t feel any hurry to change our interest rate policy,” he said.

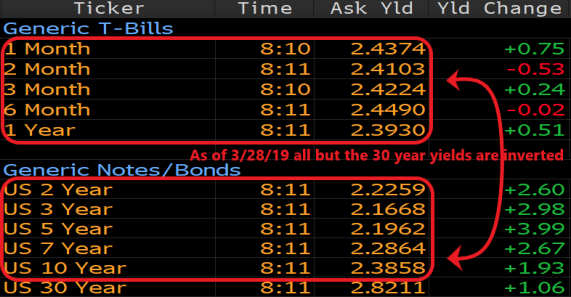

The 3M/10s part of the Treasury yield curve, which is deemed as the most reliable recession indicator, has inverted for the first time since 2007. This occurred just two days after the (Federal Open Market Committee) FOMC delivered one of the most dovish projections in recent years. As of March 28th, 2019, all long-term rates except for the 30 Year Treasury are paying less than all short-term rates, creating an almost complete inversion.

Politico, March 28th, 2019 – Mueller, charged with investigating allegations of collusion between the president’s 2016 campaign and the Russian government, returned a report to the Justice Department last week concluding that no such collusion occurred. Mueller said he was unable to come to a conclusion on whether Trump committed obstruction of justice, although Attorney General Robert Barr and deputy Attorney General Rod Rosenstein said it was their conclusion that the president was innocent of those allegations as well. In Fluent Financial’s opinion, this finding significantly reduces any instability in domestic markets from the threat of impeachment. We view the removal of this headwind as positive, but markets went down the day after the report was release and have only moved slightly higher in the days that followed.

US China trade talks have been strained recently by several events. The first was when Trump walked away from the North Korean negotiations, causing China’s Xi Jinping to fear losing face should a similar lack of agreement take place during a face to face Summit with the US President. Also, during the week of March 15th, security firms disclosed that Chinese military units have engaged in large-scale targeting of American underwater technology from universities and research institutes to boost Beijing’s naval buildup. The initial Summit between Trump and Xi Jinping was tentatively set for late March, delayed until April and has now been pushed back to June. If a deal is reached between the two countries, we would expect an initial market surge, followed by near term market declines until China proves that they will abide by the agreement.

In developed International markets, the U.K. Parliament has already rejected two Brexit agreements and blocked a vote on a third agreement, casting a shadow on a European marketplace that is already facing slowing growth. Parliament then voted on eight different proposals on March 27th that had been made as an alternative to the Withdrawal Agreement presented by PM May. All failed a majority in the Commons outright, even though they were non-binding. In other words, this low-stakes effort to try and start working towards consensus couldn’t manage to get a single plan across the line and increases the chances of a “Hard Brexit” on April 12th.

Japan’s exports fell for a third straight month in February, suggesting the BOJ might be forced to offer more stimulus to temper the effects of slowing external demand and trade frictions. Exports fell 1.2% YEAR OVER YEAR, following a sharp 8.4% YEAR OVER YEAR decrease in January, according to Bloomberg. The trade data comes on top of a recent batch of weak indicators, such as factory output and a key gauge of capital spending. The U.S. markets appear stable based on the recent 4th quarter earnings numbers but fears of slowing global growth from Japan to Europe may already be taking its toll. The S&P 500’s Q4 earnings per share grew by 12.25% compared to the same period last year, below the 15.5% estimate (according to Refinitiv data) and a possible sign that slowing global growth is already beginning to affect the U.S. markets.

WTI Crude prices are up over 30% this year to around $60/bbl. According to Jeff Klearman at Granite Shares, crude oil prices have continued to move higher through March, supported by a much-larger-than-expected decrease in U.S. inventory levels and reports Saudi Arabia intended to continue its large cutbacks. Lower Venezuelan oil exports, concerns of potential production problems in Algeria and recent drop in active U.S. rigs also supported prices at these higher levels.

In our opinion, the detailed headwinds discussed above are causing the risks of a downward move to outweigh the risks of any lost opportunities in a spike to the upside, and because of this, Fluent Financial is taking a more defensive short-term market view in the form of holding more cash and purchasing additional Put protection for certain portfolios. Additionally, any sharp upward moves may cause the Federal Reserve to rethink their passive rate hike position and take it as an opportunity to raise rates, causing a negative reaction in stocks. We still believe that the S&P 500 may provide low double digit returns in 2019 and are compelled to sit back and allow the market to catch its collective breath after an excellent first quarter of the year.

As always, please feel free to reach out with any questions. Have a wonderful weekend!

Best,

Fluent Financial Team