|

As we are looking forward to 2019, we wanted to stop and reflect on 2018. We wanted to give you the facts around what has happened over the past year and what may happen in the coming future. Although there was quite a bit of volatility in the fourth quarter of 2018, our hedging strategies limited your participation in the volatility. Please remember the Fluent Financial team is here to answer any questions or ease any of your concerns.

We wish you happy holidays and a healthy, prosperous New Year.

Here are some positive takeaways:

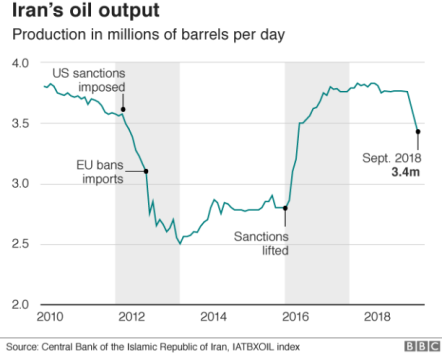

- The current oil glut is not insurmountable as Iranian oil waivers expire in May of 2019 and there should be a seasonal increase in demand for the Summer driving season. Analysts are still calling for $70 to $75 a barrel oil in 2019.

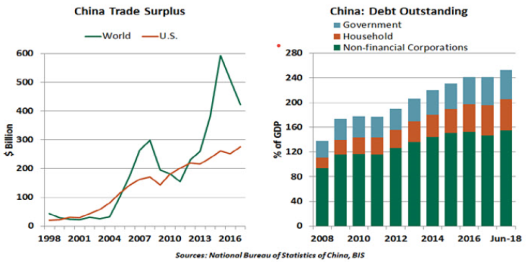

- Don’t bet against “The art of the Deal”. China has habitually violated international sanctions and Trump appears to be the first President to confront these violations in a serious manner. China is facing a slowing economy with pressure building on President Xi to make changes. Specifically, the Chinese people are looking for added production, rising wages, stronger domestic consumption, and a generally improving living standard. If you combine these factors along with other countries following Trump’s lead in confronting China, something has got to give. If and when a trade deal is made, the U.S. and International markets may see a material rebound.

- The Federal Reserve has stated that they plan to continue their rate hikes in 2019 but also seem open to adjusting this stance. The recent rate hike arguably tells investors that the Fed continues to see strong U.S. growth. Fed Chairman Powell noted that the Fed sees growth “moderating ahead” from a rising trajectory in 2018. There’s been a “tightening of financial conditions” over the last months, he added, and “weaker growth abroad.” Those are factors that helped shape the Fed’s decision to slightly lower its growth and inflation predictions for 2019. There’s an “array of diverse views” at the Fed, and that current economic conditions allow the Fed to be patient in making its rate decisions. Maybe some of the weakness in stocks following the decision had to do with the Fed’s reduced economic outlook. It now sees 3% U.S. gross domestic product (GDP) growth this year, down from 3.1% previously. It expects 2.3% GDP growth next year, down from the previous 2.5%. On the positive side, the Fed lowered its inflation outlook. It now sees 1.9% inflation in 2018, down from 2.1% previously, and 1.9% next year, down from 2%.

- International markets appear to be leveling off. According to Rida Morwa at Seeking Alpha, “International markets were the first to go into a correction territory amid concerns over global growth worries. It is good to note that some of these markets are already showing signs of leveling off.”

- The Nasdaq Index is officially in a “bear market”. The index closed on Friday (12/21/18) down 3% lower at the 6,333 level, resulting in a 21.9% drop from its all-time high of 8,109.69 hit on August 29. The widely accepted definition of a “bear market” is a drop of at least 20% from a recent peak. The S&P 500 index is down by 17% from its all-time highs recorded on September 21, 2018. So, we are about 3% away from being officially in a bear market. What is very interesting in this case is that another 3% down is a major support trendline that goes back to the year 2010. The Chart below shows the NYSE Index ($NYA) which is composed of 2,800 stocks. The trend line starts from the lows of the 2008-2009 recession and shows how close we are to this resistance support level.

Triggers for past Bear Markets include economic recessions within the U.S. or other major global players (Europe or China), an asset bubble (stocks or real estate), technology stock bubbles (2000), aggressive interest rate hikes that make bonds much more attractive than stocks and finally, spikes in commodity prices (oil) that can impact economic growth. None of the above ingredients or triggers are available. The most frequent trigger for a bear market is an economic recession. Economic recessions are scary because during recessions, companies start to struggle and post less profits. This results in a deterioration of the underlying fundamentals, and corporate profits start to decline. But this is not the situation today as this pullback is more the result of negative sentiment rather than negative fundamentals. The state of the U.S. economy is solid and enjoying a period of low unemployment and low inflation. If we do enter officially into a Bear market, it should be a relatively mild one and unlikely to last long, simply because macroeconomic factors do not support it. Remember, the current pullback has little to do with fundamentals and more to do with negative investors’ sentiment. Even if this scenario plays out, the worst of the downturn is likely to be behind us.

Downward Market Pressure events in 2018:

- Oil had a steady rise through the first nine months of 2018, hitting a high of $76.90 on October 3rd, in anticipation of Trump reinstating Iranian sanctions. Trump then unexpectedly granted waivers to eight countries (South Korea, Taiwan, Turkey, Greece, Japan, China, India and Italy) and stated his logic as “I could get the Iran oil down to zero immediately, but it would cause a shock to the market.” The markets had increased the supplies of oil throughout the world in preparation for these sanctions and once the waivers were announced, the resulting oil “glut” caused a price decline of +40% since October 3rd.

- U.S. China Trade Tariffs are causing increased volatility in the markets. China has benefited from low labor costs, largely due to the protection provided to Chinese industries in the form of lax environmental laws, generous domestic subsidies, state ownership and a “managed” currency as well as appropriations of intellectual property and discrimination against foreign firms. The U.S. is the only country to retaliate (with import tariffs) against China’s practices, but it is gaining some support. Chinese authorities have shown a limited willingness to change course, but they may be forced to be more flexible. The massive accumulation of debt across China’s economic sectors cannot be easily sustained if economic growth falters further. Things may get worse in the trade arena before they get better, but China may see wisdom in seeking a truce.

- The Fed continues to speak in aggressive terms with regards to raising interest rates and this is adding to downward pressure on stocks as this year ends. The S&P 500 Index dropped to a 15-month low on December 19th after policy makers raised rates for the fourth time this year and lowered their forecast for hikes next year to two from three. Markets had been priced for just one. Treasury yields slid, and the dollar erased losses as Powell said the Fed’s balance sheet normalization would continue “on automatic pilot.” Investors had anticipated a less aggressive approach after U.S. stocks tumbled into a correction amid concern that global growth is slowing. Amid the recent volatility in stocks and other risky assets, President Donald Trump had stepped up pressure on the central bank to avoid more tightening in the run-up to the announcement. Powell said today that political considerations play no role in Fed policy.

- Global growth appears to be slowing. Economic figures from both Europe and China on December 14 have fueled concerns that slowing global growth at the tail end of 2018 will carry over into next year. China reported soft industrial production and retail data, while a key business index in Europe fell to its lowest level in more than four years due to violent anti-government protests in France and weak manufacturing activity that has Germany struggling to rebound from a third quarter contraction. Meanwhile, Italy is on the brink of recession. The China economic data confirm that the country’s downturn deepened last month, hitting businesses and consumers. As economic growth outside the US decelerates, investors are questioning how long the US economy can withstand the global slowdown — especially since the Fed raised interest rates in their December meeting for the ninth time since the end of 2015 and the diminishing effects of the massive fiscal policy package also expected to weigh on domestic economic growth next year.

- England is having a difficult time breaking away from the EU and Italy is struggling to get their budget approved by the EU. The UK economy is suffering partially in response to fears regarding the growing risks of a no deal Brexit, a chaotic scenario that all parties claim to want to avoid. Prime Minister Theresa May is stuck between a rock and a hard place. Even her own party won’t back the Brexit deal she negotiated with Brussels. And EU officials refuse to modify the terms that were brokered in what appears to be an effort to make an example of Britain and a warning for any other EU members that are considering an exit strategy. The sticking point largely remains the treatment of the border between Ireland and Northern Ireland.

Italy’s coalition government that formed after elections in March promised voters a universal basic income, lower taxes and a reduction in the retirement age. Those plans were included in Rome’s spending plans for 2019. The proposals meant Italy would run a budget deficit of 2.4 percent for the next three years. Brussels raised concerns that Italy, with a government debt-to-GDP ratio of 133 percent already, was abandoning fiscal discipline and asked Italy to revise its spending plans. After months of disputes, Italy’s finance ministry announced a compromise with the European Union on December 18 that would target a budget deficit of 2 percent of GDP next year. If confirmed, the deal could prevent Italy from slipping into recession.

- Economic consequences from the 2018 U.S. elections will unfold. Legislatively speaking, nothing is likely to happen for the next two years. Instead of a grand bargain on a sweeping infrastructure bill or an attempt to find some comprehensive solutions to the health-care system, we’re likely to get a series of House investigations into the Trump administration and escalatory counter-punches by the president. Insofar as anything happens on the policy front, it will come unilaterally. Executive actions will be the extent of policy-making for the next two years. Trade will continue to be a focus, as will taking aim at low-hanging regulatory fruit.

In Conclusion:

According to Rida Morwa in his December 24th 2018 article A Market Bottom Could Be Very Near, “The prices of equities today are factoring a deep recession and a disaster scenario which seems unlikely to materialize.” He goes on to say that “The stock market will eventually rebound, and good stocks always bounce back. It is only a matter of ‘when’.” The argument has been made above that we could be near a bottom, which could represent a great buying opportunity before a recovery that could start at any moment.

Even in a worst-case scenario where a “bear market” materializes, it will be the result of an overshoot to the downside and not expected to last long.

The markets are currently offering tremendous opportunities in the high yield space. Current conditions, including an S&P Forward PE Ratio at approximately 14.3 (as of Dec. 19th, 2018) when it averages around 16.1, have created a great time to start picking up high quality dividend stocks on the cheap. The fear is that these current bargain valuations are unlikely to last long.

As Warren Buffet once said, “Be fearful when others are greedy and be greedy when others are fearful.” When others are greedy, prices typically boil over, and one should be cautious lest they overpay for an asset that subsequently leads to anemic returns. When others are fearful, it may present a good value buying opportunity, and this appears to be the current market situation. This summary was written with the assistance of JP Morgan, SeekingAlpha.com’s Rida Morwa, Bloomberg, Northern Trust and State Street Global Advisors research.

Looking forward to working with you in 2019,

Mitch and the Fluent Financial Team

Mitch Kramer, CFP®, MBA

Founder and CEO

|