Market Update as of May 15th, 2019

May 29, 2019Market Update as of September 5th, 2019

September 12, 2019

Fluent Financial Market Update as of July 15th, 2019

As we wind down the month of July and head into August, we want to keep you up-to-date with the market and our portfolio activity. We hope you are having a wonderful summer and as always, please feel free to reach out with any questions. We are happy to help and provide any support and additional information.

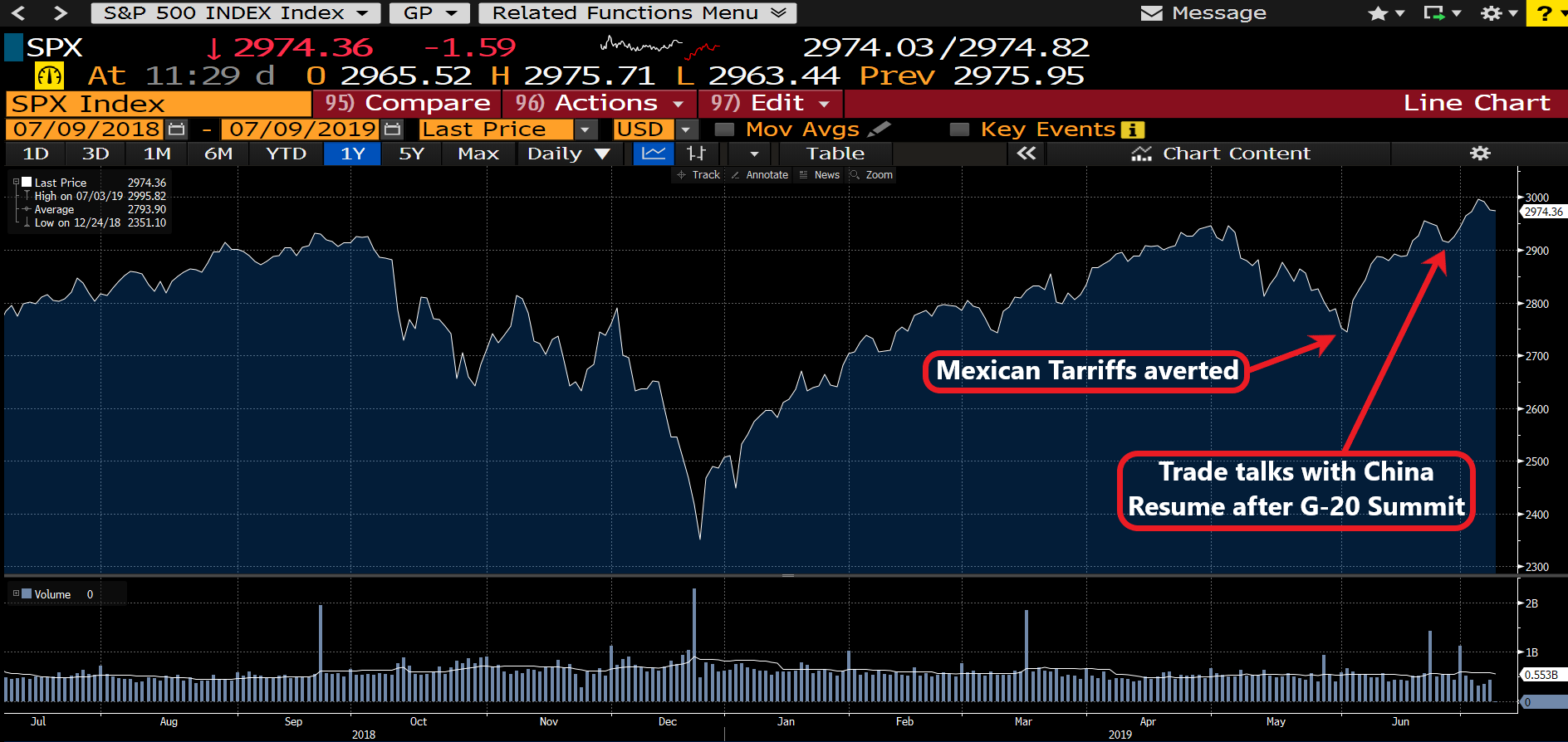

- The S&P 500 was up 6.89% (plus another 2.45% through July 12th) while the MSCI All Country World Index (ACWI) finished up 6.37% and the Barclay’s US Bond Index was up 1.26% in June

- US trade tensions with China continue as both sides returned to negotiations after the G-20 Summit

- The Fed may be forced to rethink a possible July rate cut due to recent positive jobs numbers

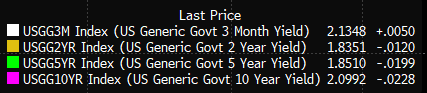

- The 3-Month/10-Year Yield curve remains inverted, a possibly recession indicator

- US Markets continue to “climb the wall of worry” and limp to new record levels

- Fluent Financial remains in a defensive posture

MARKET SUMMARY:

Markets just witnessed the best June performance since 1938 with the S&P 500 up 6.89%! This number is a bit deceiving as the S&P 500 was up only 4.3% for the quarter with the months of May (-6.58%) and June offsetting each other. The recent increases are attributed to the U.S. Mexico trade tariff threats abated, positive feelings on a U.S. China trade agreement and a more dovish Fed.

The positive sentiment that the U.S. and China would resume trade talks was confirmed over the final weekend in June, although no actual change has occurred between the two parties. Trump has agreed to hold off, temporarily, adding an additional $300 billion in Chinese tariffs as talks continue but we wouldn’t expect this to last long. China appears to be trying to wait out the Trump Presidency, hoping he is only a one term President, and Trump’s patience with China may be running thin.

As downside risks mount for both the U.S. and global economies, the discussion has shifted from the Fed hiking rates and reducing their balance sheet to fresh rounds of monetary stimulus. Analysts are slashing estimates for the 2nd half of 2019 and into 2020 on consumer consumption, business investment, and trade. While the consensus among Fed governors ranges between no rate cuts to one rate cut, the market had been pricing in far more aggressive Fed action through June and early July. Markets had been pricing in a 40% likelihood that the Fed cuts by 0.50% at their end of July meeting according to Fed Funds futures but recent positive jobs results announced July 5th have changed this assessment to either no rate changes or a 0.25% cut. The US economy added 224,000 jobs in June (160k was the estimate), bouncing back from the subpar 72,000 added in May. Unemployment rose by 0.1%, but for the right reason—labor participation ticked up. Overall, this was a strong report, suggesting that the economy is still healthy and that any rate cuts may be unnecessary.

A strong case could be made that a rate cut could be justified at the end of July as it would bring the current 3-Month/10-Year Yield curve inversion back in line. Rates for the 10-Year US Treasuries dropped below the 3-month rates (inverted) on May 22nd this year and have stayed this way ever since. Inversions like this have been a sign in the past of a possible recession but in this case, it could just be reflecting an overly aggressive Federal Reserve that raised rates one too many times in December of 2018.

PORTFOLIO SUMMARY:

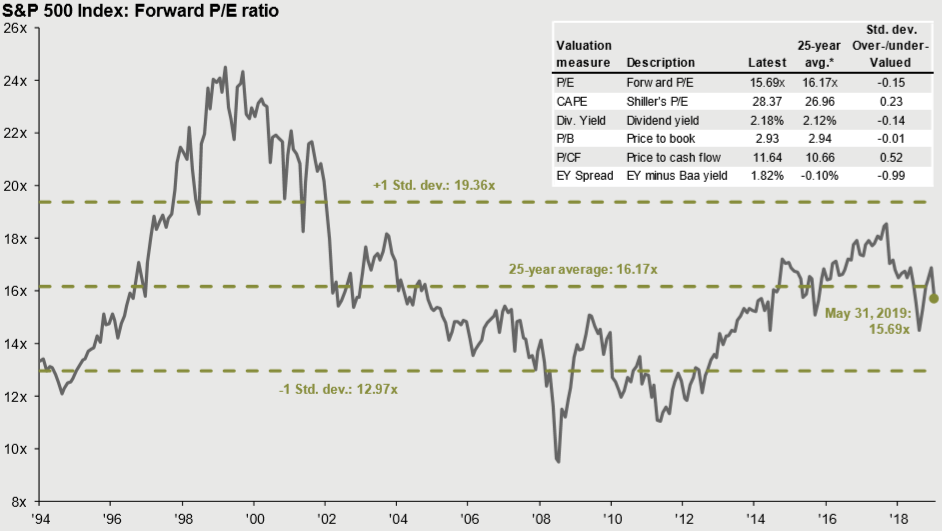

Fluent Financial’s portfolios trailed their benchmarks across the board in June but the largest discrepancy was seen in our GRO portfolio, lagging 3.61% behind our benchmark after outperforming by 2.75% in May. 3.22% of this lag was directly attributed to our two Put positions losing value and the excess cash position we had been holding. Other portfolios like ADV, ADVP and V&O suffered similar Put and cash drag scenarios while GWI and GWIM only suffered from the cash drag as they do not contain Puts. This is not an excuse for why we missed our benchmarks but rather the result of poor timing on our part. The defensive decisions we made in late February based on slowing international and domestic growth and trade dispute headwinds with China were premature in hindsight, but the S&P 500 remains at a Forward PE of 15.69, close to its 25-year historic 16.17 average. A Fed rate reduction could add temporary short-term support for this market but could also spook investors into thinking the U.S. isn’t as financially sound as previously thought. Also, with the 10-year US Treasury paying around 2% and slowing international growth, more investors may be willing to steer their money towards riskier US stocks, thus “climbing the wall of worry” and ignoring the obvious downside risks.

MOVING FORWARD:

Fluent Financial continues to believe that the market is overvalued at these levels and we will therefore continue forward with a defensive posture. We realize that stocks have hit record high levels recently but when tasked with safeguarding our client’s money, our mindset continues to be very defensive in nature and focused on maintaining gains rather than missing out on additional upside movements. In our opinion, the risk of going down 10% from these levels seems greater than the risk of missing out on another 5% upward movement. Increases like we have seen through June and early July caused temporary challenges with the performance of several of our portfolios but any slight valuation adjustment, like what we witnessed in May, will be very beneficial to our clients based on our current positions.