Mueller Report, Yield Curve Inversion, and More – What Does This Mean to You?

March 29, 2019Market Update as of July 15th, 2019

July 18, 2019

Thank you to everyone who attended our Annual Horse Race Event. We had a wonderful time catching up with everyone and getting to show our appreciation. We look forward to seeing everyone next year!

We now offer Notary services for our clients at no additional cost. Please contact Christina Zook to schedule Notary services at christina@fluentfinancial.com .

As we head towards the end of May and into June, we wanted to keep you updated on the happenings in the economy and how it relates to the market and your money.

Fluent Financial Market Update as of May 15 th , 2019

• Year-to-date, the S&P 500 is up 13.73%, the Barclay’s US Bond Index is up 3.63% and the MSCI All Country World Index (ACWI) is up 11.21%

• US trade tensions with China continue to heat up

• First quarter domestic growth was surprisingly strong

• Corporate earning slowed but still grew

• Treasury Yields were up slightly but inflation remains low

• The Federal Reserve continues to remain neutral regarding any changes to the interest rate

• Fluent Financial remains defensive on our short-term market outlook

• Tactical trading of our equity and option positions continues to yield positive performance

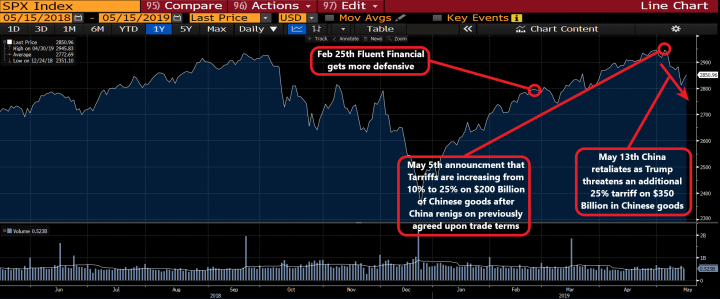

The first quarter’s stock market rally continued right through April, with all equity market segments registering gains for the month. The S&P 500 is up 12.17%, the Barclay’s US Bond Index is up 3.46% YTD and the MSCI All Country World Index (ACWI) is up 10.10% for the year. Concerns regarding an earnings recession were mitigated as Q1 earnings registered very modest gains as stronger than expected economic indicators provided a boost as well. Late in the day on Sunday May 5 th , the low volume market “melt-up” was rocked by the news that President Trump was increasing tariffs from 10% to 25% on the current $200 Billion in Chinese goods. This was in response to an almost complete retraction by the Chinese on everything trade related that had been agreed upon up to that point. In response, China increased their tariffs on US goods, causing Trump to threaten an additional 25% tariff on $350 Billion more of Chinese exports.

First-quarter GDP grew 3.2% — a substantial upside surprise given the 2.3% estimate. In addition, productivity grew at 3.6% versus an estimated 2.2% in the first quarter — the fastest growth since 2014. The first quarter usually experiences the lowest GDP of the four quarters throughout the year, so these results are giving us a bit more confidence in the domestic market that a recession is not as likely in the short term.

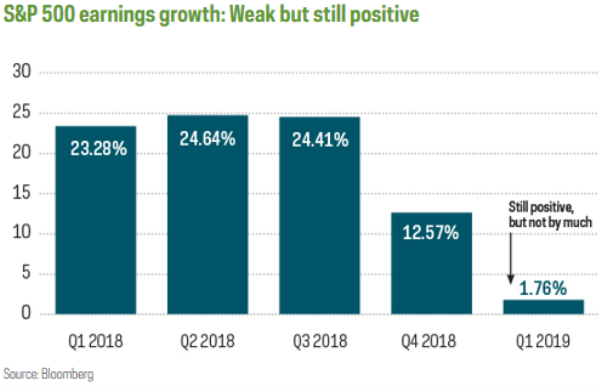

The slowdown in corporate earnings growth, one of our previously identified headwinds, appears to have begun. S&P 500 earnings growth was 1.7% in the first quarter (with roughly 90% of companies reporting), a sharp decline from the 25% growth registered for much of 2018. It’s still a positive number, however, despite many strategists forecasting an earnings recession, with actual declines in corporate earnings.

The current 2.5% yield on the 10-year U.S. Treasury seems particularly low against the backdrop of decent economic growth and low unemployment. Productivity growth may take a bit of the edge off inflation pressures, but even if inflation remains stubbornly slightly below the Fed’s target of 2%, a real yield (deducting inflation) on the 10-year Treasury of less than 1% is nearly unprecedented. Remember, if interest rates rise, bond prices fall, so long-duration bonds may be poised to underperform.

The Federal Reserve was going to raise interest rates in 2019, but the sharp decline in the stock market in Q4, concerns regarding global economic growth, and low inflation led the Fed to tilt its outlook in a considerably more dovish direction. Some began anticipating actual cut(s) in the Fed Funds rate, but Chairman Powell threw cold water on this notion by emphatically declaring the Fed’s neutral stance, suggesting that below-target inflation is likely to be transitory.

On February 25 th , Fluent Financial began taking a more defensive stance with regards to the markets as the S&P 500 was already over 10% and our predictions for the year were in the low double digits. The market continued to move higher in what can be best described as a “melt-up”. This is where investors are more scared of missing out on market gains in the face of ominous headwinds, combined with lower volumes entering into the Summer months, exacerbating any market moves. A trade deal with China seems to already be priced into the market so we would imagine that any actual announcement will cause a market pullback. We have maintained that China will continue to violate any signed agreements as they wait for a political change in the US and that this trade war is just at the beginning phase of a long and drawn out trade conflict.

Bloomberg’s SPY One Year Chart with Recent Key Events Highlighted:

The technology and trading platform at TD Ameritrade have allowed us to be more precise with our entry and exit points into stock and options positions. A recent example of this occurred on Christmas Eve, 2018, when we were able to sell some of the Puts we had purchased in SPY for a 400% gain, softening the effects of the market decline at that time. Prior to our time at TD, timely executing an exit of a position like this was unattainable. Another trading tool we use to our benefit is called a “trailing stop” order. This order type allows us to ride the gains of a position higher and dictate a point of sale if the market turns to the downside. Using this trailing stop allowed us to exit our position in Boeing (BA) around the $427 level, $13 off it’s all time high. Boeing is currently trading in the low $300s and we are continuing to wait out the bad news and look for a reentry point. Fluent Financial plans to continue using these and other tools to help maximize gains and minimize losses for our clients as we feel it is a differentiating factor in helping clients reach their financial goals.

The stock market and the economy tend to move in the same direction in the long run, and because the U.S. fundamentals are decent right now, we feel that a recession is not imminent. We also feel like the risk of a big bear market decline like 2007-2009 or 2000-2002 is low right now. Volatility can be expected to continue in the short run as China tries to hold out for someone other than Trump to be elected. In recent days when the S&P 500 went down more than 1%, our defensive positioning was on full display as our portfolios showed only fractional losses, and several of our more option heavy portfolios like ADV and ADVP registered gains. Fluent Financial will continue to invest the larger than normal cash balances during market dips and take advantage of the volatility by trading in and out of our options in a timely manner.

As always, please feel free to reach out to our office with any questions or concerns and it will be our pleasure to assist you.

Best,

The Fluent Financial Team

***This report was put together with the help of research and articles provided by SeekingAlpha.com, ProShares and Bloomberg